Understanding the Moratorium Period in Life Insurance:

When you purchase a life insurance policy, you enter into an agreement with the insurance company to protect your loved ones financially in case of your death. However, what happens if, during the early years of your policy, the insurer finds out that you didn't fully disclose important details about your health or lifestyle? This is where the moratorium period in life insurance comes into play.

What is the Moratorium Period in Life Insurance?

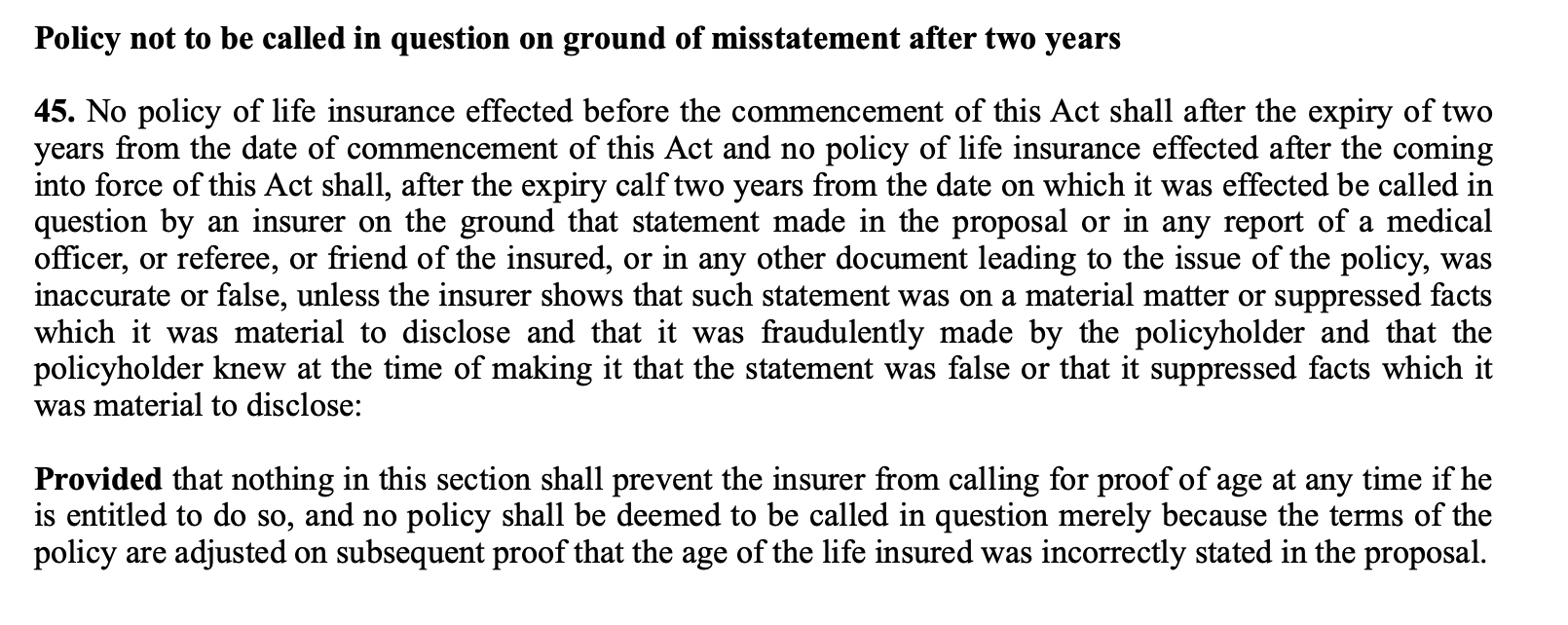

The moratorium period in life insurance refers to the time frame during which the insurer can investigate and challenge a claim if there has been misrepresentation or non-disclosure by the policyholder. In simple terms, it’s a contestability period during which the insurer can examine whether all the information you provided when buying the policy was truthful and complete.

Key Facts about the Moratorium Period in Life Insurance:

- Duration: The current moratorium period under the Insurance Laws (Amendment) Act, 2015, is 2 years from the date the policy is issued.

- Misrepresentation and Non-Disclosure: During the 2-year period, if the policyholder provides incorrect or incomplete information (like failing to disclose a pre-existing medical condition), the insurer can reject the claim.

- Fraud: If fraud is detected, the insurer can contest the policy or deny the claim at any time, even after the 2-year period.

Why Does the Moratorium Period Matter?

Think of the moratorium period as a window of time during which the insurance company is allowed to double-check that the information provided by the policyholder is accurate. If any significant facts are missed, such as a history of heart disease or smoking, the insurer can contest the policy. However, after the 2-year moratorium period, the policyholder gains protection from such challenges unless fraud is involved.

Simple Example to Understand the Moratorium Period

Let’s walk through a straightforward example to help you understand how the moratorium period works.

Scenario 1: Misrepresentation During the Moratorium Period

- Mr. Sharma buys a life insurance policy on January 1, 2023 for ₹10 lakh.

- Mr. Sharma doesn't mention to the insurer that he has a history of heart disease, which is a material fact.

- On January 1, 2024, Mr. Sharma dies due to a heart attack.

- The insurer investigates and discovers that Mr. Sharma did not disclose his heart disease. Since this was within the 2-year moratorium period, the insurer can deny the claim based on misrepresentation.

Scenario 2: After the Moratorium Period Ends

- If Mr. Sharma had passed away on February 1, 2025, the policy would have been in force for more than 2 years.

- Outcome: The insurer cannot deny the claim based on Mr. Sharma’s non-disclosure of his heart disease, because the 2-year moratorium period has passed. The insurer would have to pay the ₹10 lakh to Mr. Sharma’s family, unless fraud is proven.

Scenario 3: Fraud (Applicable Anytime)

- If Mr. Sharma intentionally lied about his health, claiming he was in perfect health when he was actually undergoing cancer treatment, this would be considered fraud.

- If the insurer finds evidence of fraud, they can reject the claim or cancel the policy at any time — even after the 2-year moratorium period.

What Happens After the Moratorium Period Ends?

Once the 2-year moratorium period has passed, the policyholder is protected from the insurer rejecting the claim for reasons of misrepresentation or non-disclosure. The insurer can no longer challenge the validity of the policy unless there is evidence of fraud.

This provides peace of mind to the policyholder, as they are not at risk of their policy being canceled or a claim being denied after the 2-year period, unless intentional fraud or an illegal activity was committed which was the root cause the death.

Why is the Moratorium Period Important for Life Insurance Policyholders?

- Protection for Policyholders: The moratorium period gives the insurer time to review the information provided during the policy application. Once this period ends, policyholders gain protection from the insurer contesting their claim due to honest mistakes or non-disclosures.

- Clarity on Misrepresentation: If the policyholder failed to disclose important facts, the insurer can cancel the policy or reject the claim within the first 2 years. This ensures that the insurance company has the opportunity to detect any issues that could affect the risk assessment.

- Security After 2 Years: After the 2-year period, the insurer cannot contest the claim or void the policy, giving policyholders security and confidence that their beneficiaries will receive the death benefit.

- Fraud Exception: If fraud is proven, the insurer has the right to reject the claim or cancel the policy at any time, regardless of the moratorium period.

Conclusion: Why the Moratorium Period Matters in Life Insurance

The moratorium period plays a crucial role in balancing the interests of both the insurer and the policyholder. It allows the insurer to ensure that all material facts have been disclosed and assessed, but also protects the policyholder after a reasonable time, preventing claims from being rejected or policies being canceled unfairly.

- For policyholders, understanding the 2-year contestability period is essential to avoid surprises and ensure that your policy remains valid.

- For insurers, it helps to manage risk and ensure that they are not providing coverage to individuals who may have misrepresented their health status or other important details.

Remember, to ensure a smooth claim process in the future, always provide accurate and complete information to your insurer when purchasing life insurance.

Key Takeaways:

- The moratorium period (or contestability period) is 2 years.

- During this period, the insurer can reject the claim due to misrepresentation or non-disclosure.

- After 2 years, the insurer cannot contest the policy unless there is fraud.

- Fraud can be detected and acted upon at any time during the life of the policy.

- Please be aware that Moratorium period will start again if you changing to a new policy (not much of a problem, but good to be aware of)

By understanding the moratorium period, you ensure a smooth life insurance experience, whether you're the policyholder or the beneficiary. This knowledge helps you make informed decisions when buying a life insurance policy, ensuring you are protected when your loved ones need it the most.

Want to know the Right Life Insurance?

or feel free to reach out at hello@honvest.com

Our certified Insurance Advisors can help you with right plan, right coverage, best premium options available

What is Moratorium period in Life Insurance?